By Andrea F. Pringle, The Baker Group

A wave of forbearance expirations expected this spring has investors anxiously awaiting clarity on what it will mean for the mortgage market. COVID-19 forbearance plans introduced by the CARES Act last year make it possible for any borrower with a mortgage backed by Fannie/Freddie/Ginnie to stop paying their loan for a maximum of 12 months due to pandemic-related hardship. The majority of loans in forbearance today entered forbearance in April 2020. With the deadlines on those loans fast approaching, what happens next is front of mind.

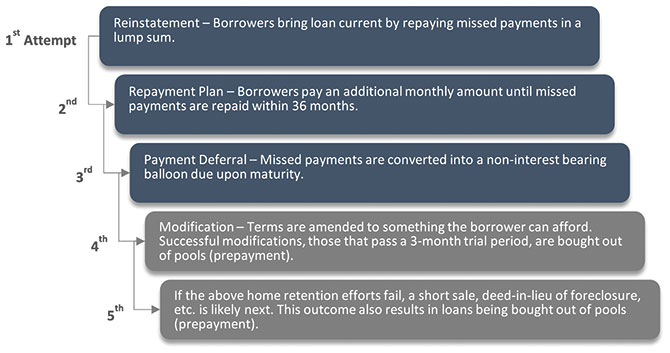

There are several paths a loan can take when forbearance expires. These paths prioritize keeping borrowers in their homes and minimizing disruption to the mortgage market. For conventional borrowers, the exit paths follow the waterfall chart. (Figure 1)

(Figure 1)

It is worth highlighting that options 1-3 all present no actual impact to MBS investors. In those expiry paths, the mortgage remains in the pool and investors continue to receive scheduled principal and interest. Only options 4 and 5 result in prepayments.

While we do not yet know how the impending expirations will ultimately play out, we can make some inferences. Forbearance plans have been available to borrowers facing natural disaster hardships for years, which gives us some historical precedence to draw from. However, there are a number of differences between forbearance today and pre-pandemic forbearance that impact borrower behavior.

While we do not yet know how the impending expirations will ultimately play out, we can make some inferences. Forbearance plans have been available to borrowers facing natural disaster hardships for years, which gives us some historical precedence to draw from.

One major difference is the root cause of forbearance. Today’s global pandemic differs from a geographically isolated natural disaster in that it affects a wider swath of the country and presents a longer path to recovery. Borrowers are staying in forbearance longer today than in the past and evidence shows that the longer a loan is in forbearance, the more likely it is to experience a credit event (short sale, deed-in-lieu, etc.). That tells us we should expect a large number of credit events as forbearance terms expire this spring. However, there are reasons to believe that loans coming out of forbearance now have a better chance of becoming current than ever before.

First, today’s housing market is particularly strong. This helps borrowers stave off credit events because they can sell their homes and pay off their mortgages in full, and has already led to substantially fewer credit events than we would otherwise expect to see. Second, the new payment deferral options introduced by the GSEs make it possible for borrowers to transition back to current without coming up with additional cash.

These conflicting factors have added to the uncertainty around what will happen when the 12-month terms start to expire. On one side of the equation, the fact that borrowers are spending a longer time in forbearance increases the likelihood of them experiencing a credit event upon expiry. On the other side, borrowers arguably have a better opportunity to avoid a credit event today because of the strong housing market and payment deferrals availability.

It is estimated that the share of loans in forbearance that will ultimately experience a credit event could be between 0.7%-7.2%. That is a wide range, but taking that percentage of roughly 5% of all mortgages currently in forbearance does not amount to an alarming share of the agency mortgage universe. Further, because these forbearance terms expire on a rolling timeline, the impact should not overwhelm the market. This is not to say there will be no impact; there undoubtedly will be, but it does suggest the disruption is likely insufficient to warrant substantial changes to investors’ strategies.