When rates were at record lows for long periods of time, the true value of low-cost funding may have faded into the background; however, low-cost core deposits continue to be the driver of long-term franchise value. Now, with rates continuing to rise — the one-year treasury exceeded 4.5% in January of 2023 — the importance of low-cost funding is once again at the forefront.

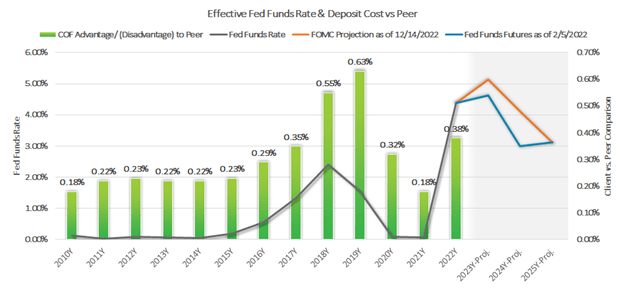

The chart below is for a financial institution with strong low- and no-cost funding. In record low-rate environments, its cost-of-funds advantage over its peers was relatively small at 20-30bp. When rates started to rise from 2017-2019, it tripled to 60bp. For a $1 billion institution, that represents a $6 million increase to the bottom line. The current rising rate environment will lead to similar increases in profit. The jump from an 18bp to a 38bp advantage in 2022 shows a trend that will continue to accelerate.

In addition, deposit growth stagnated in Q2 of 2022 and then started to decline in the second half of 2022. On the macro level, FDIC-insured deposits were down for the first time in a long time, and they were down significantly at 2.89% from their peak in Q1 of 2022. A deeper dive into the deposit decline shows that the majority of the decline happened in non-interest-bearing deposits, which declined almost 6%. That decline was partially offset by growth in growth in time and brokered deposits, putting even more pressure on funding costs. On the micro level, our data for consumer and business checking account deposit balances shows balances are down 5% and 4%, respectively, from the beginning of 2022. Even more importantly, the entire balance decline happened since mid-2022, and we anticipate this trend will continue.

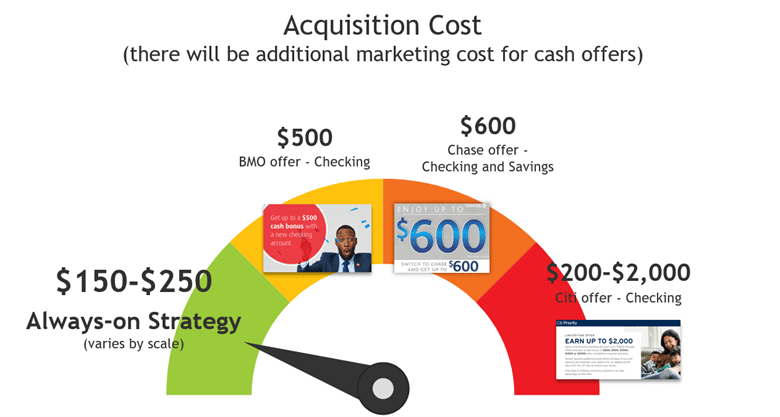

Large institutions are aware of the value created by low-cost deposits, and they have the budgets to target core relationships that drive these benefits. For example, Chase is back to its $600 offer for opening a checking and a savings account. BMO Harris pays up to $500, and Citi has an offer of up to $2,000 for relationships with extremely high balances.

In addition to the cost of the offer, these largest banks spend a significant amount of marketing dollars to gain new core relationships and the benefits that come with them. When a financial institution does not commit to an always-on marketing strategy, it must provide above-market offers to “buy” new relationships.

Community-based financial institutions (FIs) cannot compete by following a similar strategy. Unlike their large competitors, community-based FIs do not have the budgets for acquisition incentives of $500+ or the expansive budgets associated with marketing to acquire these relationships.

Compared to community-based FIs, large banks generally have more products and services as well as marketing teams who dwarf their smaller competitors. Given this reality, what does a community-based FI need to do to thrive?

To grow low-cost deposits, it is essential you follow a disciplined approach:

Step One: Your Institution Must Have a Sales and Service Culture

Good products are the foundation of a sales and service culture. You cannot ask your teams to sell or consumers to buy inferior products. If you want to know if your institution has good products, ask your customer-facing employees; they can tell you how consumers respond. Equally important is ensuring your team members are well-trained, understand and believe in your products, and consistently execute your service expectations.

Step Two: Your Institution Must Be Strategic

Large institutions have staffing and marketing budgets that allow them to change offers frequently, products marketed and/or desired prospects. For community-based FIs to compete, they must make data-driven, always-on marketing part of their core growth strategy. Your always-on marketing strategy, supported by your sales and service culture, will drive tangible results even when large banks are in periods of very high offers.

Step Three: Your Institution Must Be Aligned

Your FI’s training and execution at the branch and through online channels must be aligned with your strategic marketing. Aligning marketing and execution is what reduces the acquisition costs for new core relationships. Without this alignment, your FI is left trying to compete on the offer alone, making it expensive to match those large bank offers previously mentioned.

Step Four: Measure, Inspect and Reward!

Any strategic initiative needs to be measured. Your core relationship growth strategy should have periodic — quarterly at least — goals. In addition, determine benchmarks to evaluate success. Inspect what you expect in order to ensure your sales and service standards are being consistently executed. Reward success! When your team members are fully aware of where they stand compared to their goals, it is possible to evaluate results and reward successes.

Growing core relationships in order to grow low-cost deposits should be of primary importance in any rate environment; however, it is paramount in the current rising rate environment. Ultimately, outperforming your peers by 60bp will be welcomed by your board and celebrated by your management team. When you strategically align your culture, products, and people, competing for core relationships becomes easier, and the $500+ offers from large banks become less effective. David will beat Goliath!

Achim Griesel is President, and Dr. Sean Payant is Chief Strategy Officer at Haberfeld, a data-driven consulting firm specializing in core relationships and profitability growth for community financial institutions. Achim can be reached at (402) 323-3793 or achim@haberfeld.com. Sean can be reached at (402) 323-3614 or sean@haberfeld.com.