Many financial institution executives spend considerable time thinking about strategies to improve efficiency in order to improve overall profitability. The efficiency ratio is the ratio of noninterest expenses (less amortization of intangible assets) to net interest income and noninterest income, so it is effectively a measure of what you spend compared to what you make. The very name — “efficiency ratio” — makes us think about how efficient we are with those precious income dollars. If a financial institution has a high-efficiency ratio, they are simply spending too much of what they make … right? That is exactly what the name implies (emphasis on the spending side of the equation). But this is just a ratio of two numbers, and as we all know, there are two ways to bring the ratio down — reduce costs or increase revenues.

The focus across industry press and conference best practices is generally aimed at strategies to cut expenses — using technology, looking at staffing levels, increasing productivity, etc. Although this advice is sound, what happens when a financial institution has already cut what can be cut AND it is still struggling with efficiency? It is sometimes difficult to save your way to prosperity.

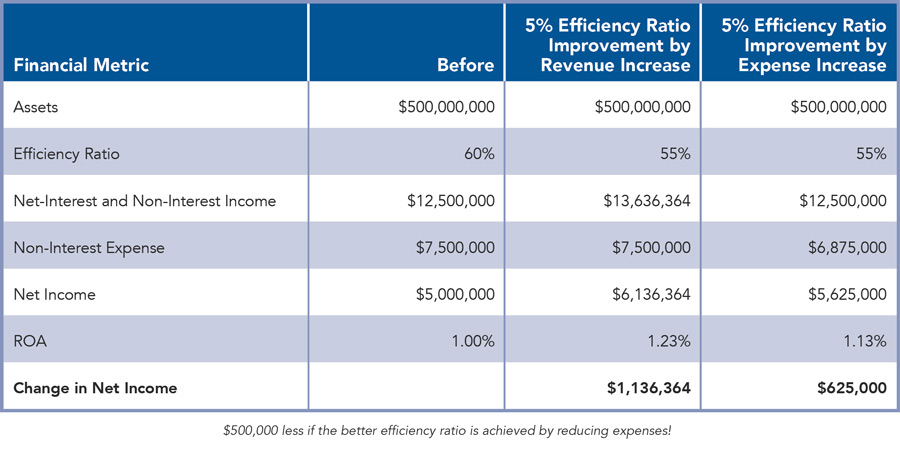

For many financial institutions, the focus should also be on the bottom portion of the equation — increasing revenues. Let’s look at an institution that has $500 million in assets, a good return at 1% ROA and a reasonable efficiency ratio of 60%. Let’s assume the FI can improve its efficiency ratio by 5% through revenue increase or expense reduction.

It shouldn’t be surprising that increasing revenues provides better performance, even though this sometimes seems like a counterintuitive approach. Because many financial institutions need to increase investments for growth in order to significantly grow their revenues, thereby increasing the expense side of the equation, and because of their excess capacity, this will actually make them more efficient over time. Many financial institutions have cut expenses almost to the bone and can’t materially improve their efficiency ratio by further reducing costs. They need to take a step back and realize some fundamental business dynamics that are often ignored in our industry.

Most community financial institutions still have tremendous excess capacity, meaning they could serve significantly more customers without significantly increasing expenses. The answer to improving the efficiency ratio is to fill excess capacity with brand NEW profitable customers.

How do other businesses look at the issue of excess capacity — for example, a manufacturing company?

- The facility is running at 50% of the capacity it was built to produce;

- The factory has done everything it can to be as efficient as possible — evaluate staffing levels, implement technology solutions, etc.; and

- Management’s major goals and objectives are still focused on improving profitability by further evaluating already efficient processes and selling more to current customers.

Given the excess capacity at the manufacturing company, wouldn’t it also make sense to evaluate if more widgets can be run through the facility? Would the market support providing more products to more people in order to increase net income without substantially increasing expenses?

The manufacturing company analogy is very similar to the situation being faced by community financial institutions. Their branches currently attract 30% to 50% of the new customers they were built to serve each year, and the situation is getting worse as transaction volume continues to decline in branches. Most financial institutions have used technology and staff reductions to become more efficient; however, they still spend much of their time, effort and energy focusing on cost reductions and additional efficiency enhancement.

When a community financial institution starts welcoming significantly more new customers per year, fixed costs do not substantially change — no new branches have been built, no additional employees have been hired. Actual data from hundreds of community financial institutions illustrates the impact on actual expenses is just the marginal costs — generally an additional $30-$50 per account per year (even if we must mail a paper statement). Conversely, the same database shows that the average annual contribution of each new account per year is between $250 and $350.

When comparing clients that have embraced this strategy to the overall industry over a three-year period of time (2014 to 2017), their improvement in efficiency ratio was 63% better. This has been accomplished by significantly increasing the number of new customers coming in the front doors of existing branches.

There is only so much blood in a turnip. Controlling costs, embracing technology to reduce process costs and evaluating staffing are all things financial institutions should be doing; however, if they have already become very efficient in these areas, the focus must shift to driving revenue. Most financial institutions have tremendous excess capacity in their existing branches today. The solution is to start filling them up.

Sean C. Payant, Ph.D., is the chief strategy officer at Haberfeld, a data-driven consulting firm specializing in core relationships and profitability growth for community-based financial institutions. Sean can be reached at (402) 323-3614 or sean@haberfeld.com.