As the U.S. economy continues to work its way out of the recession brought on by the COVID-19 pandemic, many economists debate what the future will hold. With inflation, asset bubbles, rising rates, and the effect of fiscal spending being hot topics during board and ALCO discussions, the question becomes this: What should we do to prepare our balance sheet for what may come? However, for all these discussions about potential future challenges to earnings, seldom do boards and ALCOs discuss the revenues lost due to opportunity cost.

Opportunity cost lurks as a silent killer of margins, especially given the current abundance of liquidity in financial institutions. While tax returns and stimulus checks continue to add to the excess of liquidity, the earnings on those dollars remain at near zero. With all the uncertainty in the economy, many financial institutions fall victim to sitting on the sidelines waiting for a clearer picture to emerge and are missing out on the current opportunity the market is giving them.

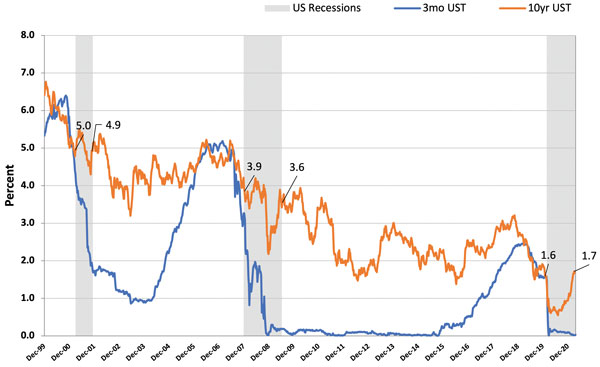

3-Month UST vs. 10-Year UST

While the official start of the current recession was February 2020, the downturn in economic activity began much earlier with the Federal Reserve acting quickly to soften the blow and lower rates. The drop in short-term rates was quick. The 10yr treasury followed suit, dropping from 1.60% at the start of the recession to a low of 0.55% by August 2020. Following that low, the 10yr started moving higher and currently sits around 1.60% at the time of this writing, a significant level given the behavior of past recessions.

Upon the beginning of recovery following the previous two recessions, the 10yr regained its pre-recession levels and saw minimal gains from that point. At the same time, short-term rates continued to either decline or remained lower for a prolonged period. The early 2000s recession, known as the dot-com bubble, saw the 10yr at 5.00% and eight months later hit 4.90% at the recession’s official end. During the Great Recession, which lasted more than twice as long, the 10yr entered at 3.90% and hit around 3.60% at the beginning of the subsequent recovery.

In both cases, the 10yr saw most gains initially jump to start the recovery, with very little if any increase beyond that. While the current recession is ongoing, the 10yr has already reached its pre-recession levels. With Federal Reserve pledging to continue keeping rates low, the opportunity for financial institutions to recoup lost margins is now.

The best way we can tackle both the pressures of future economic uncertainty and opportunity costs is to actively manage the risks to our balance sheet through sound asset-liability management. While many will claim they already do this, the fact remains that a large number of financial institutions only manage parts of their balance sheet, leaving others on autopilot. The best-performing institutions take advantage of all the tools available to properly manage risks regardless of what the economy and interest rates are doing.

Stabilizing Funding

One of the most significant fears examiners have put into financial institutions is the idea that without warning, we may face a large run-off in our deposit portfolios. All too often this fear causes many institutions to overcompensate by holding on to more liquidity than is necessary. Looking at current call report data as deposits soar to record levels once again, many institutions find themselves questioning whether this liquidity is here to stay or is on the way out as quickly as it arrived.

Maintaining excess cash levels to have sufficient liquidity is not only inadequate risk management, it is also the most expensive method from an opportunity cost standpoint. Proper liquidity management means having adequate cash flows and contingent liquidity sources to meet any loan demand or deposit withdrawals.

The better performing institutions tend to use opportunities in wholesale funding from a source such as the Federal Home Loan Bank. With borrowing rates remaining low, the opportunity exists to make a positive spread on loans. So rather than waiting for loan demand to use our excess cash, we can now deploy those funds to avoid lost income due to opportunity cost. In the worst case, if we are short on funds when loan demand comes in, we can borrow and still maintain positive margins.

Managing and Diversifying Loans

In a similar way to deposits, loans often fall victim to an autopilot management style where loan demand ebbs and flows based both on volume and the types of loans, with seemingly little we can do about it. In reality, the loan portfolio can be diversified and managed similarly to the investment portfolio through loan participation. Selling loans can help us to manage excess flows in a particular loan type, alleviating concentration risk while also generating some off-balance-sheet revenue through servicing income.

Purchasing loan participations can help fill the gaps in the loan portfolio where retail demand falls short, allowing us to diversify the loan portfolio and potentially hedge against prepayment or geographic risks. The relevant example is the large amount of refinancing seen recently in the mortgage market, which caused mortgage-heavy institutions to experience faster than expected turn-over in their loan portfolios, resulting in a loss of income.

Investment Portfolio Management

Perhaps the biggest victim of opportunity cost is the investment portfolio, especially during rising rates and the effect of falling market values. Frequently, boards and ALCOs will put these unrealized losses on investments under a microscope and pause to purchase more investments while seeking to understand what has happened. However, we tend to ignore the fact that the drop in valuation also affects our loans, a big part of interest rate risk, but more importantly, this is generally good for the balance sheet as a whole.

Lower market values on our investments mean there is an opportunity for maturing investments to move into higher rates, allowing our portfolio income to grow and cash invested at a higher spread. The current investments will continue to generate revenue for us and, unless we choose to sell them before maturity, that loss will eventually disappear as the investment matures.

No one can predict precisely where the economy will go from here and waiting to get a clear direction will only cause us to fall victim to opportunity cost. The only way to adequately address these uncertainties is to have solid asset-liability management and take advantage of all the available tools to cultivate a well-diversified balance sheet and actively managed it across deposits, loans, and investments. In this way, we ensure that we manage our institutions to the risks we know instead of the unknowns.

Greg Tomaszewicz is a Senior Financial Strategist with The Baker Group. Before joining the firm in 2018, Greg spent 12 years working for a fixed-income broker/dealer in New York. He helped financial institutions across the country evaluate their balance sheet risks and opportunities. In addition, he worked to develop new analytics to aid those clients in meeting the challenges of an ever-changing economic environment. Greg holds a bachelor’s degree in economics from Stony Brook University. Contact Greg at

(800) 937-2257 or gregt@GoBaker.com.